Дослідження "Доступне авто"

Дослідження "Доступне авто"

-

Публікації

-

Ми пишемо простими словами про складне

-

-

Калькулятори

Калькулятори

-

Симулятор бюджетів

Симулятор бюджетів

-

Бюджет України

Бюджет України

- Підтримати

Ціна популізму

Імпорт природного газу — це великі валютні витрати, а тому і вагомий фактор тиску на гривню. Від 2006 до 2015 року на імпортний газ було витрачено 87,9 млрд дол. США. Для порівняння: наш державний і гарантований борг становить всього 66.6 млрд дол. США (серпень 2016). Постає питання: що відбувалося б із зовнішніми рахунками та, відповідно, з обмінним курсом гривні, якби ринкові ціни на газ запровадили ще 2004 року?

Припущення аналізу:

- для оцінок валютного курсу ми припускаємо, що все, окрім торгового балансу, залишається так, як воно було в реальності (інвестиції, політичні рішення, структура економіки тощо);

- для оцінок потенційного видобутку газу за умови ринкової ціни припускаємо, що всі додаткові доходи від ринкової ціни інвестують у видобуток;

- ринкова ціна газу – це середня фактична ціна імпорту природного газу за період;

- курсова політика НБУ залишається без змін, і до 2014 року Нацбанк дотримується режиму фіксованого курсу;

- у розрахунках не беруть до уваги потенційний вплив від запровадження енергоефективних технологій;

- припускаємо, що за ринкової ціни на природний газ його споживання було б у середньому на 4.0 млрд м3 менше на рік.

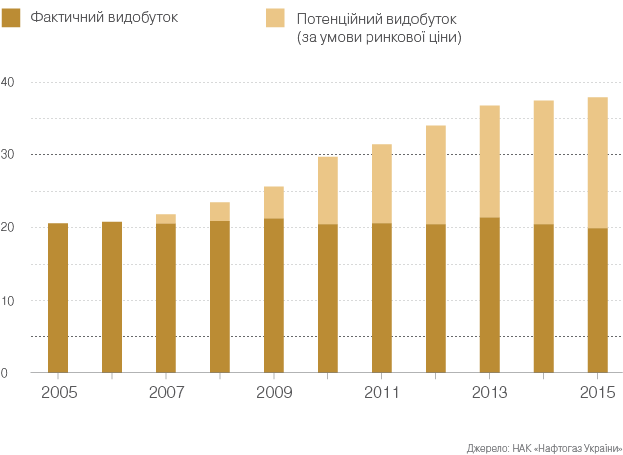

Перший наслідок — ріст видобування власного природного газу. За оцінками НАК «Нафтогаз України», за умови запровадження ринкових цін 2004 року, вже 2015 року власний видобуток сягнув би 38,0 млрд м3, а це навіть більше, аніж нам потрібно. Наприклад, торік Україна спожила всього 33,7 млрд м3, а це означає, що надлишки можна було б експортувати.

Потенційний видобуток природного газу в Україні, млрд м3

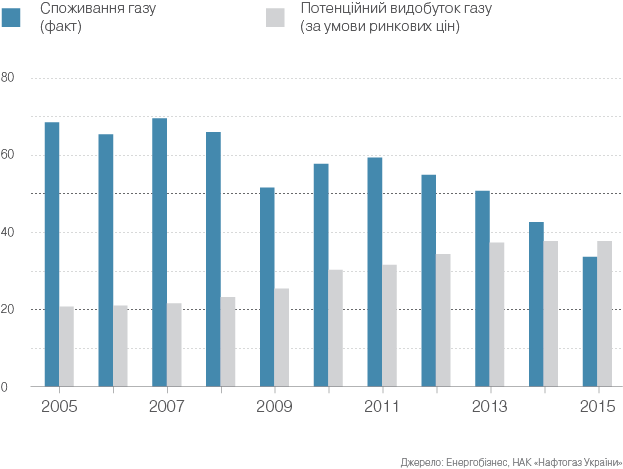

Другий наслідок — скорочення споживання природного газу. Відповідно до дослідження «Газ для домогосподарств в Україні: ринок відсутній», авторства The Oxford Institute for Energy Studies, за умов ринкової ціни, споживання природного газу скорочується мінімум на 5,7 млрд м3. Якщо інвестують в енергоефективність — споживання може знизитися додатково на 0,9–3,0 млрд м3.

Споживання природного газу vs. потенційнийвнутрішній видобуток, млрд м3

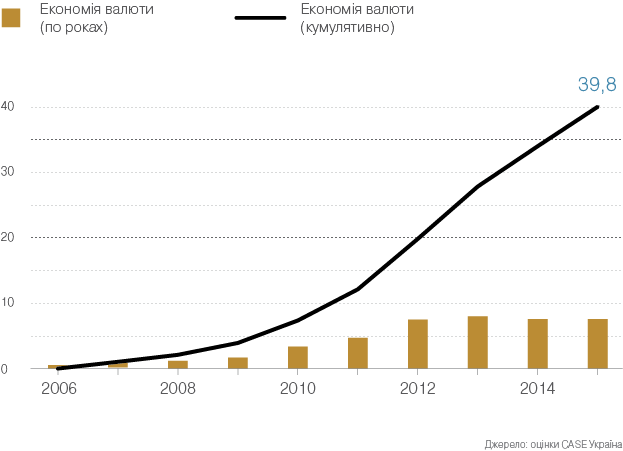

Третій наслідок — суттєва економія валюти. Навіть якщо припустити, що споживання газу буде падати не так стрімко, як пише The Oxford Institute for Energy Studies, а жодної енергоефективності не відбувається, то економія валюти, за ринкової ціни на газ, дуже велика: за нашими оцінками – близько 40 млрд дол. США з 2006 до 2015 року. Для порівняння: наші валютні резерви на сьогодні становлять усього 15.6 млрд дол. США (кінець вересня 2016).

Економія валюти від запровадження ринкових цін на газ,млрд дол. США

Як би склалося наше життя, якби не занижені внутрішні ціни на газ? Зразу можна сказати, що від валютного шоку 2008 року ринкова вартість газу нас би не врятувала. Колапс на зовнішніх ринках не залишав жодного шансу для маленьких відкритих економік, як наша. Однак у 2014–2015 роках ситуація могла б розвиватися зовсім за іншим сценарієм.

По-перше, за ринкових цін на природний газ у нас зростали б валютні резерви і на кінець 2013 року становили б вражаючі 48 млрд дол. США (5,9 місяця імпорту) порівняно з 20,4 млрд дол. США (2,5 місяця імпорту) фактичних резервів. По-друге, дефіцит зовнішньої торгівлі був би зовсім інший – за нашими підрахунками, дефіцит поточного рахунку був би всього 4.6% ВВП (8,5 млрд дол. США) порівняно з 9,0% ВВП (16,5 млрд дол. США), які ми досягли перед валютним шоком 2014 року. За таких умов і інвестиційна активність (приплив іноземного капіталу), і самі політичні рішення були б зовсім іншими (навряд чи Віктор Янукович за таких резервів відмовився б від євронітеґрації). Однак для наших оцінок валютного курсу ми припускаємо, що все, окрім торгового балансу, залишається так, як воно було в реальності.

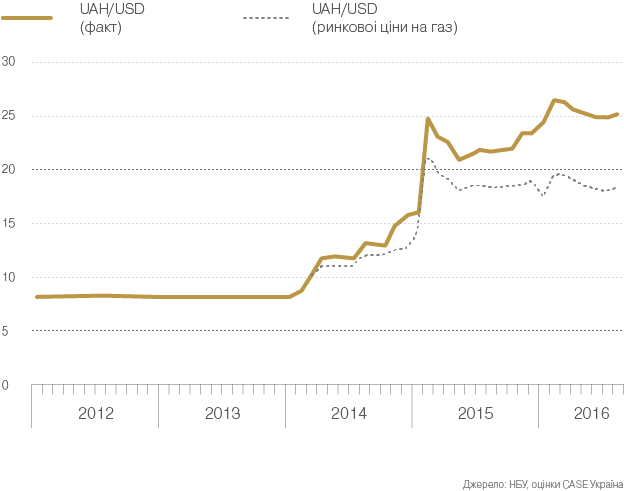

Отже, скільки коштувала б гривня, якби не газові субсидії? За нашими оцінками, після окупації частини країни та фактичного розриву економічних відносин з Росією гривня зупинилася б на позначці UAH 18.5/USD. Девальвації уникнути не вдалося б, оскільки експортний виторг стрімко падав через геополітичні процеси, однак:

- НБУ зміг би активніше «заливати» ринок валютою, маючи у розпорядженні вдвічі більші резерви (відплив валюти 2014 року становив всього 13.3 млрд дол. США порівняно з 48 млрд дол. США гіпотетичних резервів);

- великі резерви (та інтервенції) стримували б спекулятивну атаку населенням і відплив валюти з банківської системи, що зберегло б велику частину банківської системи;

- сам розмір торгового дефіциту був би вдвічі менший, що полегшувало б завдання. Окрім того, жодного імпорту газу з Росії 2015 року вже не було б, оскільки внутрішнє видобування повністю забезпечувало б наші потреби.

За таких умов 2–3% ВВП дефіциту рахунку поточних операцій – це той рівень, на якому можна було б зупинити падіння гривні. За нашими оцінками, звуження дефіциту до такого рівня досягається за UAH 11/USD 2014 року та за UAH 18.5/USD 2015 року.

Іншими словами, якби не занижені ціни на газ, середня місячна зарплата сьогодні була б не 200, а близько 300 дол. США. Середня пенсія була б не 66, а близько 100 дол. США. Багато українців зберегли б свої заощадження. І це вже не згадуючи про енергоефективність та інвестиційну привабливість, які приносять нові робочі місця та стимулюють ріст доходів. Тому вибір у нас досить простий: або низькі ціни на газ, або все-таки стабільна економіка з відкритими можливостями розвиватися та заробляти для всіх.

Обмінний курс гривні

Ми робили дуже спрощені розрахунки, не враховуючи різноманітні взаємозв’язки, як-от вплив ринкових цін на газ на структуру економіки, потенційні інвестиції в різні сектори тощо. У процесі аналізу стало зрозуміло, що ринкові ціни мали б набагато ширший позитивний ефект, окрім самого обмінного курсу гривні. Однак цю частину аналізу ми залишаємо для подальших досліджень.